Are you on the hunt for the best bank independent CD rates to grow your savings securely? Certificates of Deposit (CDs) have long been a popular choice for individuals seeking a low-risk investment option with predictable returns. Independent banks and credit unions often offer competitive CD rates compared to larger financial institutions, making them an attractive option for savvy savers. Whether you're planning for a major life event, building an emergency fund, or simply looking to maximize your savings, understanding the nuances of independent CD rates can help you make an informed decision.

Independent banks pride themselves on personalized customer service and tailored financial products, including CDs. These institutions often provide higher interest rates because they aim to attract deposits to fund their local lending operations. With the current economic climate and fluctuating interest rates, locking in a competitive CD rate from a reputable independent bank can be a smart financial move. This article dives deep into the world of independent CD rates, exploring how they work, what factors to consider, and how to find the best options available.

As you navigate the landscape of independent bank CD rates, it’s essential to weigh the pros and cons of different terms, penalties, and features. From short-term CDs that offer flexibility to long-term options with higher yields, independent banks provide a variety of choices to suit your financial goals. By the end of this guide, you’ll have a comprehensive understanding of how to identify the best bank independent CD rates and make the most of your savings. Let’s get started!

Read also:Exploring The World Of Man Cartoon Characters From Classics To Modern Icons

Table of Contents

- What Are Independent CD Rates and Why Do They Matter?

- How to Find the Best Bank Independent CD Rates?

- Factors Affecting CD Rates: What You Need to Know

- Short-Term vs. Long-Term CDs: Which Is Better for You?

- Are Online Banks Better for Independent CD Rates?

- What Are the Penalties and Fees Associated with CDs?

- How Can CD Ladders Help Maximize Returns?

- Frequently Asked Questions About Best Bank Independent CD Rates

What Are Independent CD Rates and Why Do They Matter?

Certificates of Deposit (CDs) are time-bound savings accounts that offer a fixed interest rate over a specified term. Independent banks, often smaller and community-focused, issue CDs as part of their suite of financial products. These institutions typically offer higher CD rates compared to national banks because they rely on customer deposits to fund their operations. Understanding what independent CD rates entail is crucial for anyone looking to grow their savings in a low-risk environment.

Independent CD rates are influenced by several factors, including the Federal Reserve’s interest rate policies, the bank’s financial health, and market competition. When the Federal Reserve raises interest rates, banks often increase their CD rates to attract more deposits. Conversely, during periods of low interest rates, CD rates may decrease. Independent banks, however, often maintain competitive rates even in challenging economic conditions, making them a reliable option for savers.

Why do independent CD rates matter? For starters, they provide a predictable return on your investment, which is especially appealing in uncertain economic times. Unlike stocks or mutual funds, CDs are insured by the FDIC (Federal Deposit Insurance Corporation) up to $250,000, ensuring your money is safe. Additionally, independent banks often offer perks such as higher rates for longer terms or special promotions for new customers, making them an attractive choice for maximizing your savings.

How to Find the Best Bank Independent CD Rates?

Finding the best bank independent CD rates requires a bit of research and strategy. With so many options available, it’s important to know where to look and what to consider. Start by comparing rates from multiple independent banks and credit unions. Online tools and rate comparison websites can help you quickly identify the top contenders. Keep an eye out for promotional rates, which may offer higher returns for a limited time.

Here are some steps to guide your search:

- Identify Your Goals: Determine how long you can commit your funds and what return you hope to achieve.

- Check Local Banks: Independent banks in your area may offer competitive rates tailored to community members.

- Explore Online Options: Many online-only banks provide higher CD rates due to lower overhead costs.

- Read the Fine Print: Understand the terms, including early withdrawal penalties and renewal policies.

- Consider Relationship Benefits: Some banks offer higher rates if you have other accounts with them.

Another tip is to negotiate with the bank. While not all institutions allow this, some may be willing to match or beat a competitor’s rate to win your business. By taking the time to shop around and compare offers, you can secure the best bank independent CD rates that align with your financial goals.

Read also:Show Me The Upside Down Smiley Interpretations And A Deeper Look

Factors Affecting CD Rates: What You Need to Know

Several factors influence the CD rates offered by independent banks. Understanding these elements can help you make informed decisions and anticipate changes in the market. One of the most significant factors is the Federal Reserve’s monetary policy. When the Fed raises interest rates, banks often follow suit by increasing their CD rates. Conversely, when rates are lowered, CD rates may decline as well.

Another important consideration is the term length of the CD. Generally, longer-term CDs offer higher interest rates compared to shorter-term options. This is because banks are willing to reward you for locking in your money for an extended period. However, longer terms also mean less liquidity, so it’s essential to balance your need for access to funds with the potential for higher returns.

Other factors include:

- Market Competition: Banks compete for deposits, and higher rates can be a way to attract customers.

- Economic Conditions: Inflation, unemployment rates, and overall economic health can impact CD rates.

- Bank Size and Type: Smaller, independent banks often offer better rates than larger national banks.

By staying informed about these factors, you can time your CD investments strategically and maximize your returns. For example, if you anticipate interest rates rising in the near future, you might opt for a shorter-term CD to take advantage of higher rates later.

Short-Term vs. Long-Term CDs: Which Is Better for You?

When choosing a CD, one of the most critical decisions is whether to opt for a short-term or long-term option. Short-term CDs typically have terms ranging from a few months to a year, while long-term CDs can extend up to five years or more. Each option has its advantages and drawbacks, depending on your financial goals and risk tolerance.

Short-term CDs offer greater flexibility and liquidity. If you anticipate needing access to your funds soon or expect interest rates to rise, a short-term CD might be the better choice. However, the trade-off is that these CDs generally offer lower interest rates compared to their long-term counterparts. They are ideal for individuals who prioritize flexibility over higher returns.

On the other hand, long-term CDs provide higher interest rates and the opportunity to lock in a favorable rate for an extended period. These CDs are suitable for individuals who have a long-term savings goal and can afford to part with their money for several years. However, they come with stricter penalties for early withdrawal, which can erode your earnings if you need to access the funds prematurely.

Pros and Cons of Short-Term CDs

- Pros: Flexibility, lower penalties, opportunity to reinvest at higher rates.

- Cons: Lower interest rates, less predictable returns.

Pros and Cons of Long-Term CDs

- Pros: Higher interest rates, predictable returns, long-term growth potential.

- Cons: Less liquidity, higher penalties for early withdrawal.

Are Online Banks Better for Independent CD Rates?

Online banks have revolutionized the banking industry by offering competitive rates and convenient services. When it comes to CDs, online banks often outshine traditional brick-and-mortar institutions, including independent banks. This is primarily due to their lower overhead costs, which allow them to pass on the savings to customers in the form of higher interest rates.

One of the key advantages of online banks is their ability to offer nationwide access to their CD products. This means you can compare rates from banks across the country, increasing your chances of finding the best bank independent CD rates. Additionally, online banks often have fewer fees and more flexible terms, making them an attractive option for tech-savvy savers.

However, there are some drawbacks to consider. Online banks may lack the personal touch and community involvement that independent banks provide. Additionally, some people may feel uneasy about banking entirely online, especially when it comes to managing large sums of money. Ultimately, the decision depends on your preferences and priorities.

What Are the Penalties and Fees Associated with CDs?

While CDs are a safe and reliable investment option, they come with certain penalties and fees that you should be aware of. The most common penalty is for early withdrawal, which occurs when you access your funds before the CD’s maturity date. This penalty can vary depending on the bank and the CD’s term length, but it often involves forfeiting a portion of the interest earned.

Here’s a breakdown of common penalties:

- Short-Term CDs: Penalties may range from a few months’ worth of interest.

- Long-Term CDs: Penalties can be more severe, sometimes equal to six months or more of interest.

Other fees to watch out for include account maintenance fees and renewal penalties. Some banks automatically renew your CD at maturity, often at a lower rate. To avoid this, make sure to monitor your CD’s maturity date and take action accordingly.

How to Minimize Penalties?

To minimize penalties, consider the following strategies:

- Choose a CD with a grace period after maturity to decide your next steps.

- Opt for a no-penalty CD if flexibility is a priority.

- Plan your finances to avoid the need for early withdrawals.

How Can CD Ladders Help Maximize Returns?

CD laddering is a popular strategy for maximizing returns while maintaining liquidity. The concept involves dividing your investment into multiple CDs with staggered maturity dates. For example, instead of investing $10,000 in a single five-year CD, you could split it into five $2,000 CDs with terms of one, two, three, four, and five years. As each CD matures, you can reinvest the funds into a new five-year CD, ensuring a steady stream of returns.

This strategy offers several benefits:

- Diversification: Reduces risk by spreading your investment across multiple terms.

- Liquidity: Provides access to a portion of your funds regularly.

- Higher Returns: Allows you to take advantage of higher rates for longer-term CDs.

CD laddering is particularly useful in a rising interest rate environment, as it enables you to reinvest at higher rates as each CD matures. It’s a smart way to balance security, growth, and flexibility in your savings strategy.

Frequently Asked Questions About Best Bank Independent CD Rates

What Are the Best Bank Independent CD Rates Available Today?

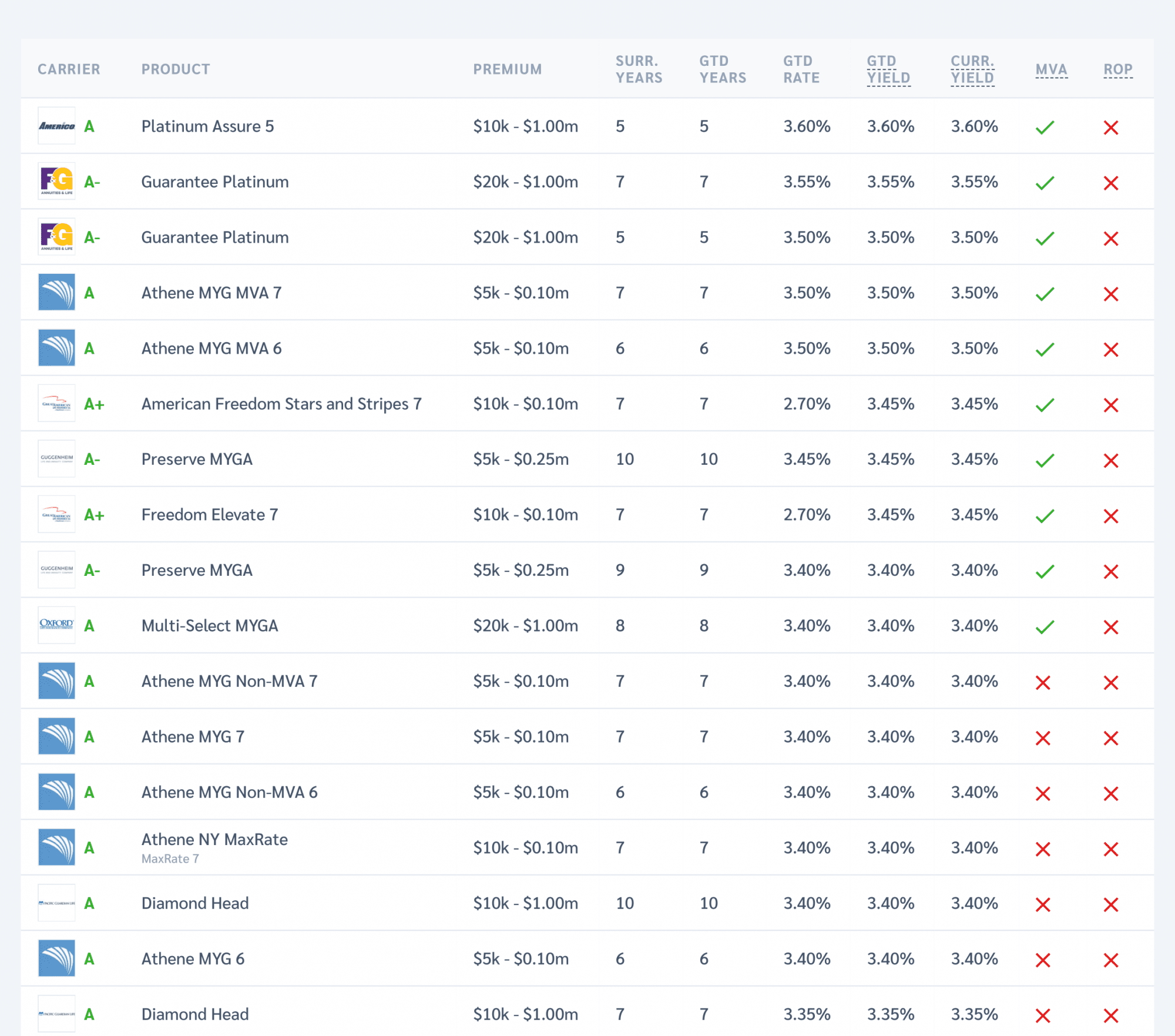

The best bank independent CD rates vary depending on the term length and the institution. As of the latest data, online banks and credit unions often lead the pack with competitive rates. For example, a one-year CD might offer an APY of 4.5%, while a five-year CD could reach 5.0% or higher. It’s essential to shop around and compare rates to find the best option for your needs.

Are Independent Bank CD Rates Higher Than National Banks?

Yes, independent banks and credit unions typically offer higher CD rates compared to national banks. This is because smaller institutions rely more heavily on customer deposits to fund their operations. Additionally, they often have lower overhead costs, allowing them to pass on the savings to customers in the form of higher interest rates.

Can I Negotiate CD Rates with Independent Banks?

In some cases, yes. While not all banks allow rate negotiations, some may be willing to match or beat a competitor’s rate