The APR reflects not only the interest rate but also any additional fees associated with the loan, giving you a clearer picture of the total borrowing cost. With so many factors influencing the APR, it’s crucial to delve deeper into how it works, why it matters, and how you can secure the best rate possible. For many car buyers, the APR can seem like a complex and intimidating concept. However, it’s essentially a standardized way to compare loan offers from different lenders. While the interest rate represents the cost of borrowing the principal amount, the APR includes additional charges such as origination fees, processing fees, and other costs. This makes the APR a more accurate measure of the true cost of financing your vehicle. By understanding what is apr rate on a car, you can avoid hidden expenses and ensure you’re getting a fair deal. Whether you’re shopping for a new or used car, the APR will directly affect your monthly payments and the total amount you’ll pay over the life of the loan. As we explore the intricacies of APR rates on cars, this article will provide a detailed breakdown of everything you need to know. From how APR is calculated to tips for lowering your rate, we’ll cover the essential aspects of this critical financial term. By the end of this guide, you’ll have a comprehensive understanding of what is apr rate on a car and how to use this knowledge to your advantage. Whether you’re preparing to buy your dream car or simply want to be a more informed consumer, this article will equip you with the tools and insights to navigate the car-buying process with confidence.

Table of Contents

- What is APR Rate on a Car?

- How is APR Calculated?

- What Factors Affect Your APR?

- Why Does APR Matter?

- How Can You Get a Lower APR?

- What Are the Differences Between APR and Interest Rate?

- How Does APR Impact Your Monthly Payments?

- FAQs About APR Rates on Cars

What is APR Rate on a Car?

At its core, the APR, or Annual Percentage Rate, is a standardized way to express the cost of borrowing money to finance a car. When you take out a car loan, the APR encompasses not only the interest rate charged by the lender but also any additional fees associated with the loan. These fees may include origination fees, processing charges, and other costs that vary depending on the lender. By bundling these costs into a single percentage, the APR provides a clearer and more accurate representation of the total cost of financing your vehicle.

Understanding what is apr rate on a car is particularly important because it allows you to compare loan offers on an apples-to-apples basis. For example, two lenders may offer the same interest rate, but one may have higher fees, resulting in a higher APR. This makes the APR a critical tool for evaluating which loan option is truly the most affordable. Additionally, the APR helps you anticipate your financial obligations over the life of the loan, ensuring there are no surprises when it comes to monthly payments or the total amount you’ll repay.

Read also:Unveiling The Truth Behind The Strawberrytabby Leaked Controversy

It’s worth noting that the APR is not a fixed value and can vary based on several factors, such as your credit score, the loan term, and the lender’s policies. A lower APR generally indicates a more affordable loan, but it’s essential to consider the bigger picture. For instance, a loan with a low APR but a shorter term may result in higher monthly payments, even if the total cost is lower. By understanding what is apr rate on a car, you can make informed decisions that align with your financial goals and budget.

How is APR Calculated?

The calculation of APR involves a combination of the interest rate and any additional fees associated with the loan. While the exact formula can vary slightly depending on the lender, the general process begins with determining the nominal interest rate, which is the base rate charged on the loan. This rate is then adjusted to include fees such as origination charges, processing fees, and other costs. The result is expressed as an annualized percentage, making it easier for borrowers to compare different loan offers.

To better understand how APR is calculated, consider this example. Let’s say you’re financing a car worth $25,000 with a nominal interest rate of 5% and additional fees totaling $1,000. The APR would take into account both the interest and the fees, spreading them over the term of the loan. If the loan term is five years, the APR might come out to approximately 6.2%, reflecting the true cost of borrowing. This figure gives you a more accurate sense of what you’ll pay over time compared to the nominal interest rate alone.

While the math behind APR can seem complex, many online calculators and tools are available to simplify the process. These tools allow you to input details like the loan amount, interest rate, fees, and term to quickly estimate the APR. By understanding how APR is calculated, you can better evaluate loan offers and ensure you’re not overlooking hidden costs. This knowledge empowers you to make smarter financial decisions and avoid loans with unnecessarily high APRs.

What Factors Affect Your APR?

Several key factors influence the APR you’ll receive when financing a car. Understanding these variables is crucial for securing the best possible rate and minimizing your overall borrowing costs. Below, we’ll explore the most significant factors that lenders consider when determining your APR.

Your Credit Score: How Does It Influence APR?

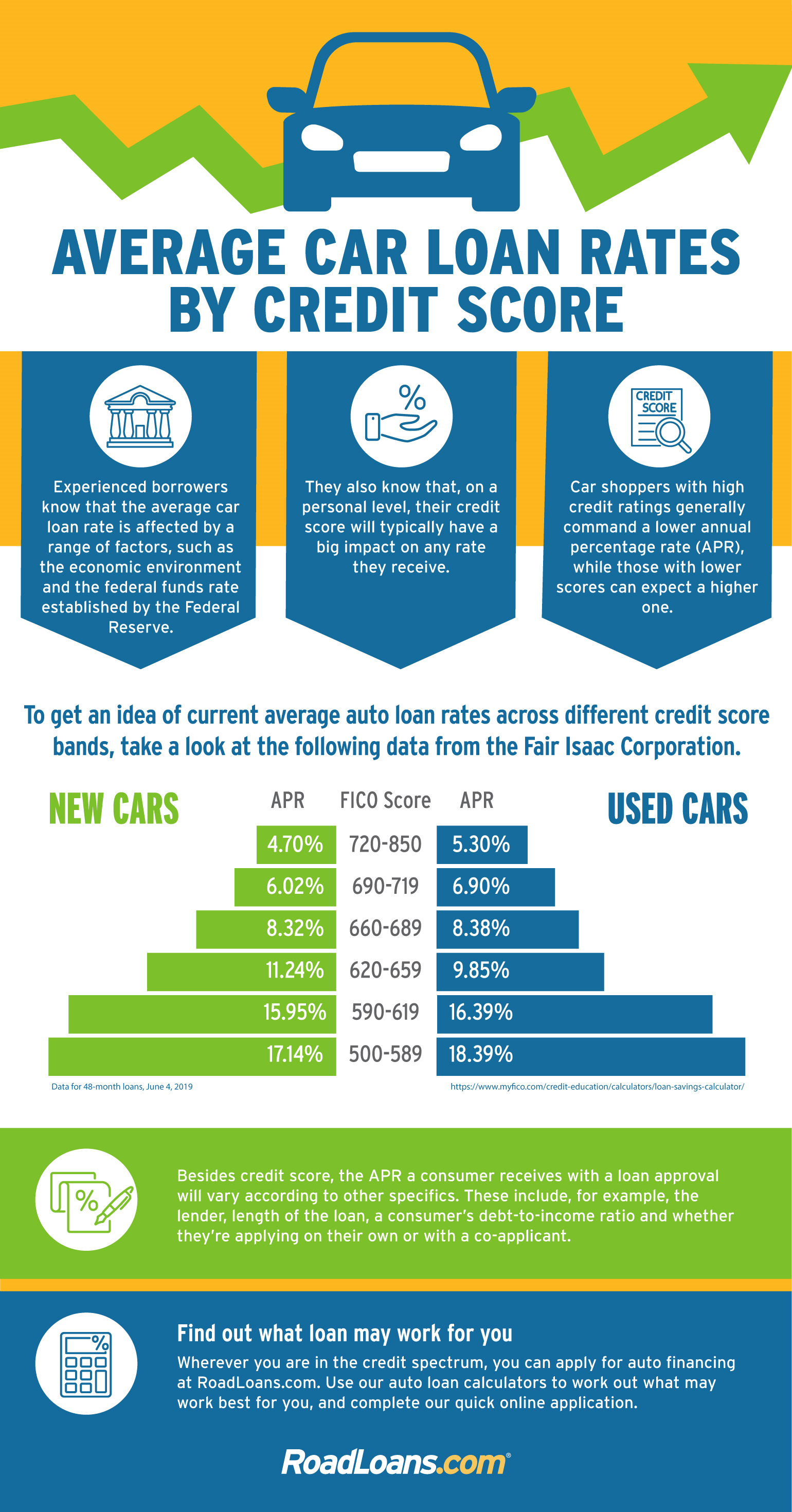

One of the most critical factors affecting your APR is your credit score. Lenders use your credit score to assess your creditworthiness and determine the level of risk involved in lending to you. A higher credit score typically results in a lower APR, as it signals to lenders that you’re a responsible borrower with a history of repaying debts on time. Conversely, a lower credit score can lead to a higher APR, as lenders may view you as a higher-risk borrower. For example, someone with a credit score above 750 might qualify for an APR of 3%, while someone with a score below 600 could face an APR of 10% or more.

Read also:Why A Nissan Frontier Used 4x4 Should Be Your Next Adventure Vehicle

Loan Term: Does a Longer Term Mean a Higher APR?

The length of your loan term also plays a significant role in determining your APR. Generally, shorter loan terms come with lower APRs, as lenders face less risk over a shorter repayment period. However, longer loan terms may result in higher APRs due to the increased uncertainty and potential for default over an extended period. For instance, a 36-month loan might have an APR of 4%, while a 72-month loan for the same amount could have an APR of 6%. While longer terms may reduce your monthly payments, they often lead to higher overall costs due to the increased APR.

Other Factors to Consider

- Down Payment: A larger down payment can reduce the loan amount, potentially lowering your APR.

- Type of Vehicle: New cars often qualify for lower APRs compared to used cars, as they are considered less risky collateral.

- Lender Policies: Different lenders have varying criteria for setting APRs, so it’s worth shopping around for the best offer.

By understanding what factors affect your APR, you can take proactive steps to secure a more favorable rate. Whether it’s improving your credit score, opting for a shorter loan term, or making a larger down payment, these strategies can help you reduce your borrowing costs and save money over the life of your loan.

Why Does APR Matter?

Understanding why APR matters is crucial for anyone navigating the car-buying process. The APR serves as a comprehensive measure of the cost of borrowing, providing a clear picture of what you’ll pay over the life of the loan. Unlike the interest rate, which only reflects the cost of borrowing the principal amount, the APR includes additional fees and charges, making it a more accurate indicator of the loan’s true cost. This distinction is particularly important when comparing multiple loan offers, as two loans with the same interest rate can have significantly different APRs due to varying fees.

One of the primary reasons APR matters is its impact on your monthly payments and total repayment amount. A higher APR means you’ll pay more in interest and fees over time, which can strain your budget and limit your financial flexibility. For example, a loan with a 5% APR might result in monthly payments of $400, while a loan with a 10% APR for the same amount could increase your payments to $450. Over the course of a five-year loan, this difference can add up to thousands of dollars in additional costs. By prioritizing loans with lower APRs, you can reduce your financial burden and make more informed decisions.

Additionally, the APR plays a critical role in helping you avoid hidden fees and unexpected expenses. Lenders are required to disclose the APR, ensuring transparency and allowing you to compare offers on an equal footing. This makes it easier to identify loans with excessive fees or unfavorable terms. By focusing on the APR, you can avoid predatory lending practices and ensure you’re getting a fair deal. Ultimately, understanding why APR matters empowers you to take control of your finances and make choices that align with your long-term goals.

How Can You Get a Lower APR?

Securing a lower APR can save you a significant amount of money over the life of your car loan. Fortunately, there are several strategies you can employ to improve your chances of obtaining a more favorable rate. Below, we’ll explore actionable steps you can take to reduce your APR and make your car financing more affordable.

Improving Your Credit Score: What Steps Should You Take?

One of the most effective ways to lower your APR is by improving your credit score. Lenders view borrowers with higher credit scores as less risky, which often translates to better loan terms and lower APRs. Start by reviewing your credit report for errors and disputing any inaccuracies. Paying down existing debt, making timely payments, and avoiding new credit inquiries can also boost your score. Even a small increase in your credit score can result in a significantly lower APR. For example, raising your score from 650 to 700 might reduce your APR from 7% to 5%, saving you hundreds or even thousands of dollars over the loan term.

Negotiating with Lenders: Can You Bargain for a Better Rate?

Another way to secure a lower APR is by negotiating directly with lenders. Many borrowers don’t realize that APRs are often negotiable, especially if you have a strong credit profile or multiple loan offers to compare. Start by gathering quotes from multiple lenders to understand the range of available APRs. Armed with this information, you can approach lenders and request a better rate. Highlighting your creditworthiness, offering a larger down payment, or opting for a shorter loan term can strengthen your negotiating position. In some cases, lenders may also offer promotional rates or discounts for customers who meet specific criteria, such as being a first-time buyer or a member of a loyalty program.

Additional Strategies to Lower Your APR

- Shop Around: Compare offers from banks, credit unions, and online lenders to find the best APR.

- Consider a Co-Signer: If your credit score is less than ideal, a co-signer with strong credit can help you qualify for a lower APR.

- Opt for a Shorter Loan Term: While shorter terms may increase your monthly payments, they often come with lower APRs and reduce the total cost of borrowing.

By taking proactive steps to improve your financial profile and negotiate effectively, you can secure a lower APR and save money on your car loan. These strategies not only make your loan more affordable but also empower you to make smarter financial decisions.

What Are the Differences Between APR and Interest Rate?

While the terms "APR" and "interest rate" are often used interchangeably, they represent two distinct aspects of a car loan. Understanding the differences between APR and interest rate is essential for making informed financial decisions. The interest rate refers solely to the cost of borrowing the principal amount, expressed as a percentage. It does not account for any additional fees or charges associated with the loan. For example, if you take out a $20,000 car loan with an interest